The Federal Reserve is entering a new phase as Kevin Warsh prepares to reshape inflation policy, rate cuts, and the future of monetary policy.

Every trader has a sky above their head.

That sky is the Federal Reserve.

And right now, that sky is about to change.

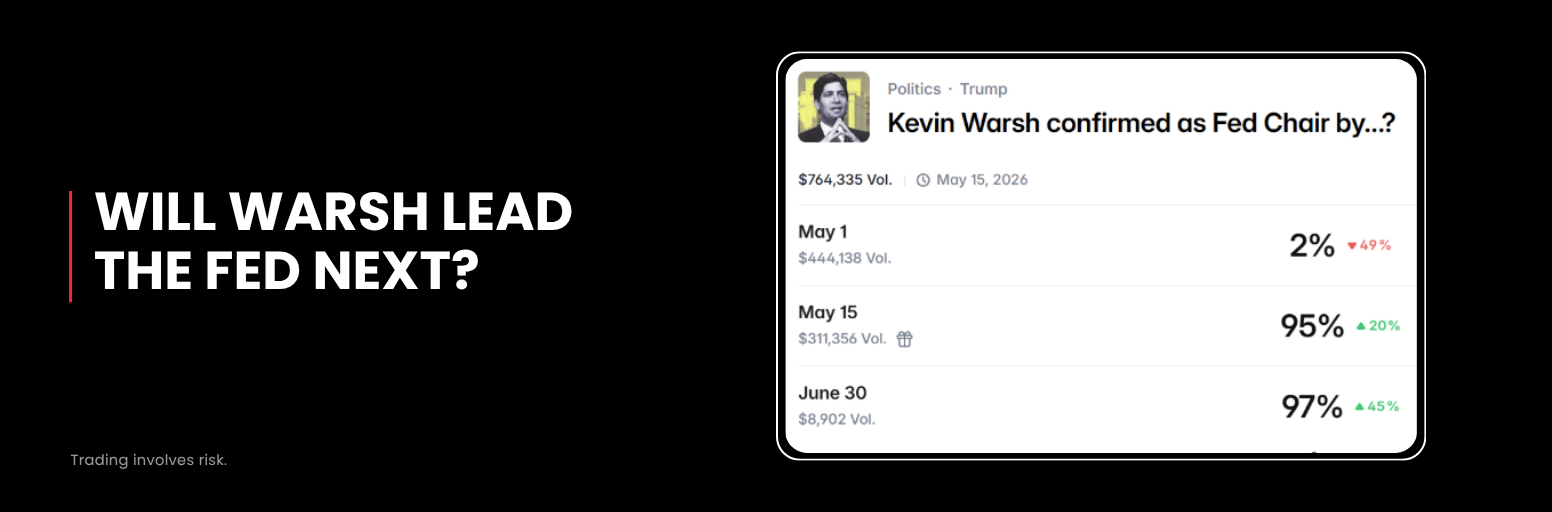

In just a few weeks, Jerome Powell is expected to step down. The market is already looking ahead to his likely successor:

Kevin Warsh.

Ambitious, reform-driven, and willing to challenge the status quo, Warsh may not just adjust policy.

He may reshape how the Fed operates entirely.

So what does that mean for inflation, rate cuts, and markets?

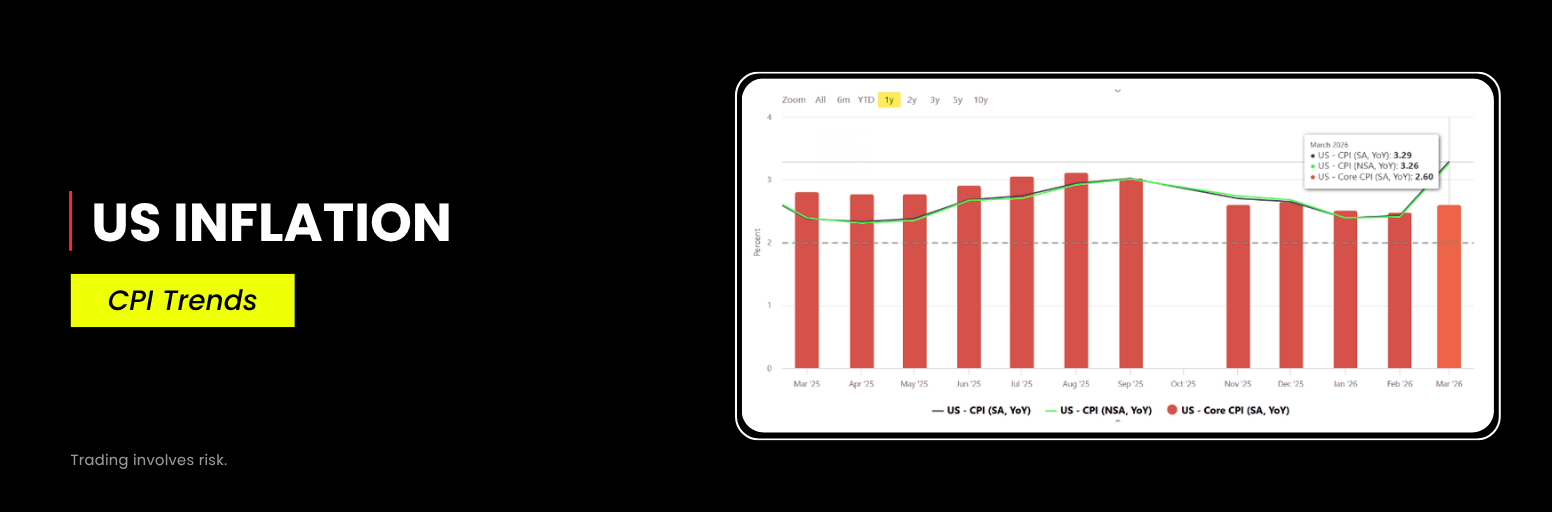

1. A Lower Tolerance for Inflation

If Powell defined the past cycle, Warsh may define the next.

The first shift is clear: lower tolerance for inflation.

“Inflation Is a Choice”

During his April 21 congressional hearing, Warsh made his stance clear.

Inflation, in his view, is not primarily driven by external shocks such as oil prices. It is the result of policy decisions.

He pointed directly to the Federal Reserve’s actions in 2021 and 2022. At the time, supply chains were already under pressure from the pandemic. Continued monetary easing added further fuel, allowing inflation to become entrenched. Once that happens, the cost of restoring stability rises significantly.

Rethinking the 2% Target

Warsh also questioned the strict 2 percent inflation target.

In his view, there is no meaningful difference between 2.0 percent, 1.9 percent, or 1.8 percent in real economic terms. However, the Fed’s rigid focus on a precise number has contributed to policy errors.

When inflation was slightly below target, the Fed continued easing. That decision helped set the stage for the inflation surge that followed.

Hawk or Dove? Neither

At first glance, Warsh’s comments sound hawkish.

But the market reaction tells a different story.

He has not positioned himself as either a hawk or a dove. Instead, he emphasizes policy flexibility and objectivity.

Monetary policy, in his view, should respond to real economic conditions:

- If inflation rises, tighten policy

- If inflation falls, ease policy

No fixed stance. No rigid guidance.

A Shift in Communication

This approach could change how the Fed communicates with markets.

Under Warsh, forward guidance may become less prominent. Instead of signaling future moves, the Fed may react more directly to incoming data.

For markets, this implies:

- Less predictability

- Faster repricing

- Greater sensitivity to economic data

2. The Core Idea: Balance Sheet First, Rate Cuts Later

One of Warsh’s most important ideas is often misunderstood.

He proposes combining balance sheet reduction with future rate cuts.

The Strategy

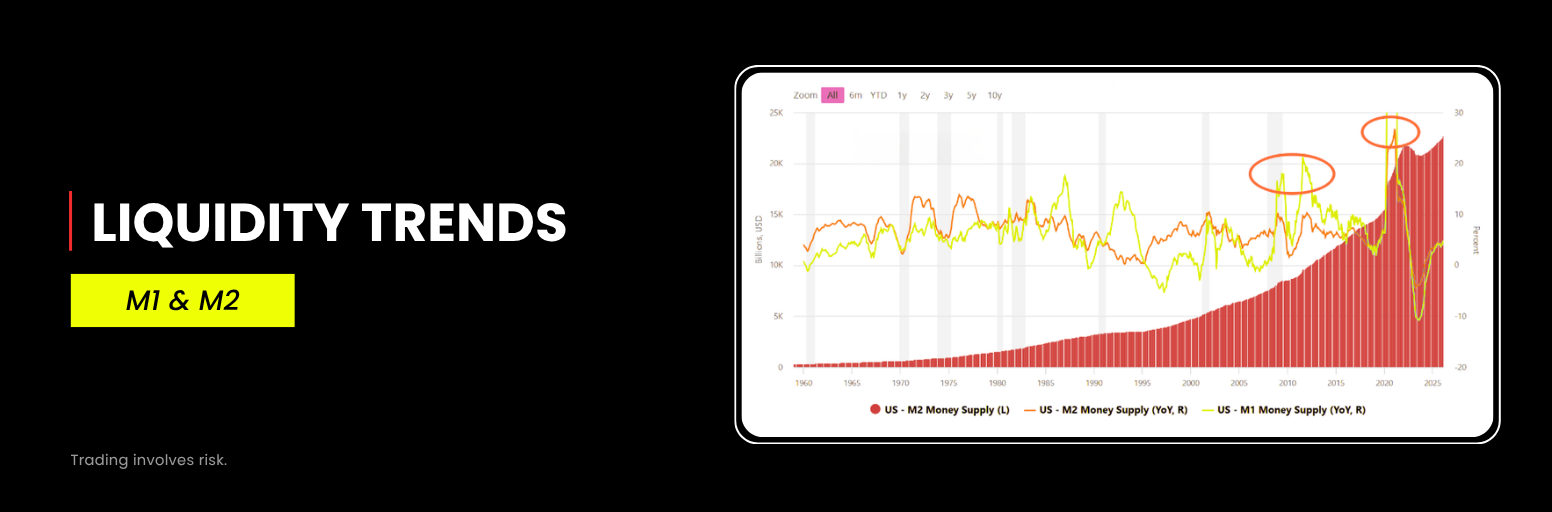

Warsh believes that reducing the Fed’s balance sheet can create room for rate cuts.

For every one trillion dollar reduction in bond holdings, there may be capacity for approximately 50 basis points of rate cuts.

At first glance, this appears dovish.

But the logic is structural.

Looking Back: 2008 and 2020

Warsh traces today’s challenges back to two key periods:

- Quantitative easing after the 2008 financial crisis

- Massive liquidity injections during the 2020 pandemic

These policies expanded the Fed’s balance sheet and significantly increased the money supply. They also blurred the line between monetary policy and fiscal support.

The Consequences

The side effects are now clear:

- Persistent inflation

- Reduced policy flexibility

- Increased dependence on central bank support

With inflation rising again, partly driven by energy prices linked to US–Iran tensions, these structural issues have become more visible.

Warsh’s Objective

Warsh’s goal is not simply to tighten policy.

It is to reset the system.

- Restore Federal Reserve independence

- Separate monetary policy from fiscal pressures

- Rebuild long-term policy flexibility

The Key Insight

Warsh is not trying to be a hawk.

He is trying to create room for future rate cuts.

But before that can happen, inflation and structural imbalances must be addressed.

3. Reality Check: Implementation Challenges

While Warsh’s framework is clear, execution will not be easy.

He Still Needs to Take Office

A congressional hearing does not guarantee appointment.

Warsh will need:

- political support

- institutional backing

- alignment within the broader policy environment

Markets assign a high probability to his appointment, but it is not certain.

A Difficult Macro Environment

Even if he takes office, the timing is challenging.

- Inflation is rising again

- Oil prices remain elevated

- US–Iran tensions are unresolved

These factors limit how quickly policy can shift.

Debt and Fiscal Pressure

The US continues to face:

- large fiscal deficits

- heavy debt issuance

A rapid reduction in the balance sheet could create instability in financial markets.

Banking System Adjustments

Warsh has also proposed loosening banking regulations to help absorb the impact of balance sheet reduction.

However, this requires coordination across multiple agencies and may take up to a year to implement.

Short-Term Market Impact

In the near term:

- Balance sheet reduction is likely to come first

- Rate cuts may be delayed

Markets may also hear more hawkish messaging as the Fed prioritizes inflation control.

The Bigger Shift in Fed Policy

The most important change is not a specific policy move.

It is a shift in philosophy.

From Guidance to Reaction

Under Powell, the Fed relied heavily on forward guidance.

Under Warsh, the approach may become more reactive.

Policy decisions may be driven more directly by economic data, rather than pre-communicated expectations.

What This Means for Markets

This shift implies:

- Increased volatility

- Faster market adjustments

- Greater importance of real-time data

Markets will need to adapt to a system with less signaling and more uncertainty.

Final Insight

The sky above the market is changing.

Not because rates will move immediately, but because the framework behind those decisions is evolving.

And when the framework changes, markets do not simply react.

They reprice everything.

Risk Disclosure

Trading in Securities, Futures, contracts for difference (CFDs) and other financial products carries high risks due to the rapid and unpredictable fluctuation in the value and prices of these financial instruments. This unpredictability is due to the adverse and unpredictable market movements, geopolitical events, economic data releases, and other unforeseen circumstances. You may sustain substantial losses including losses exceeding your initial investment within a short period of time.

You are strongly advised to fully understand the nature and inherent risks of trading with the respective financial instrument before engaging in any transactions with us. When you engage in transactions with D Prime, you acknowledge that you are aware of and accept these risks.

Disclaimer

This article may contain speculative statements regarding future expectations, plans, or projections based on information and assumptions currently available to D Prime. Although D Prime considers these assumptions reasonable, such statements involve risks, uncertainties, and factors beyond D Prime’s control, and actual outcomes may differ significantly. D Prime and its affiliates give no assurance that any views, projections, or forecasts will materialize.

This information contained in this article is for general informational and educational purposes only and should not be considered as financial, investment, legal, tax or any other form of professional advice, recommendation, an offer, or an invitation to buy or sell any financial instruments. The content herein, including but not limited to data, analyses and market commentary, is presented based on internal records and/or publicly available information and may be subject to change or revision at anytime without notice and it does not consider any specific recipient’s investment objectives or financial situation. Past performance references are not reliable indicators of future performance.

D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained in this article. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment. You should conduct your own research and consult with an independent qualified financial advisor or professional before making any financial trading or investment decisions.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.